New dues system

All farm businesses must submit an annual income tier declaration by June 30 of the current year. Were you unable to submit your declaration on time? As an exception, the declaration Website remains accessible. Access the declaration site This link will open in a new window.

A long-awaited reform

In recent years, the UPA has received a number of requests from producers to make the dues system more equitable for all farm businesses.

Following a rigorous consultation process, a resolution of intent was passed at the General Congress in December 2025, involving significant changes to the current dues system.

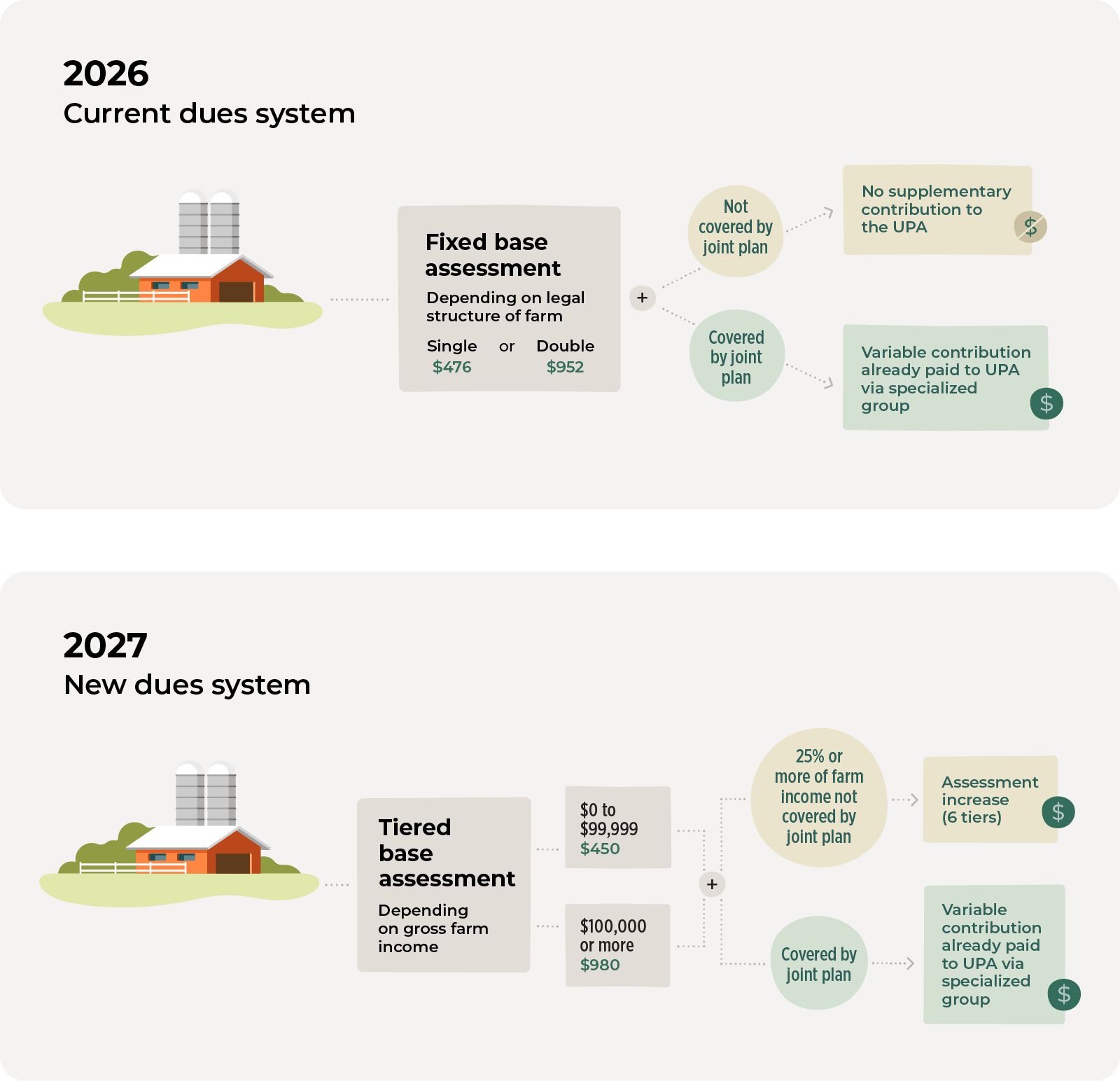

Starting in 2027, to ensure greater equity, the amount of the annual assessment will no longer be set according to the legal status of businesses. Instead, it will be determined based on gross farm income. It will also consider if the businesses already pay a contribution to the UPA through their joint plan or not.

Read more about the current dues system This link will open in a new window

Important changes

1. Tiered base assessment

The current system of single and double assessments, which are charged depending on the legal status of each farm business, will be eliminated. Starting in 2027, a new base assessment amount will apply; this amount will depend on which tier the farm falls into, based on gross income.

Prospective scenario

| Tier | Gross farm income | Base assessment | ||

|---|---|---|---|---|

| 1 | $0 to $99,999.99 | $450 | ||

| 2 | $100,000.00 or more | $980 | ||

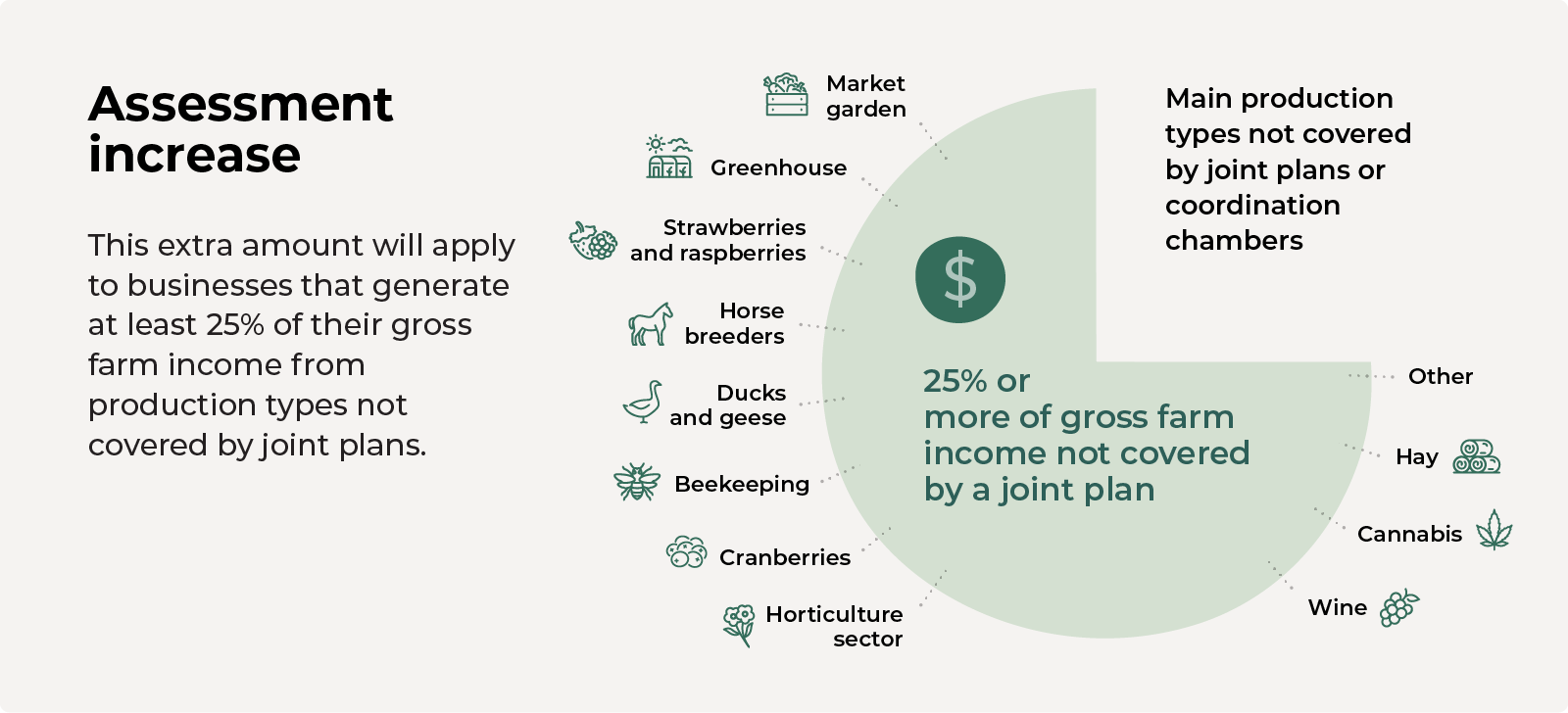

2. Assessment increase

An assessment increase (commonly referred to as a supplementary assessment) will also apply in certain cases to ensure more equity between production types that pay contributions to the UPA through joint plans and those that do not.

Will be required to pay this amount : only businesses in which at least 25% of gross farm income is generated by products not subject to contributions (87 KB) to the UPA (PNACs). The amount will be calculated based solely on gross farm income from products that are not covered by any joint plan.

When they receive their notice of dues, producers may request an alternative calculation for the assessment increase in lieu of a fixed tier (provided it receives approval from the Régie des marchés agricoles et alimentaires du Québec). To do so, they must provide official proof of their business income. In this case, the increase will be calculated at $0.95 per $1,000 increment of gross farm income not covered by joint plans.

Prospective scenario

| Tier | Gross farm income from PNACs | Assessment increase (“supplementary assessment”) | ||

|---|---|---|---|---|

| 1 | $0 to $99,999.99 | $50 | ||

| 2 | $100,000 to $249,999.99 | $175 | ||

| 3 | $250,000 to $499,999.99 | $375 | ||

| 4 | $500,000 to $999,999.99 | $750 | ||

| 5 | $1 million to $1,999,999.99 | $1,500 | ||

| 6 | $2 millions or more | $2,500 | ||

Production types covered by joint plans already pay this portion of the UPA’s financingThis link will open in a new window through contributions collected by their specialized federations and syndicates.

- Les Producteurs de lait du Québec (dairy)

- Fédération des producteurs forestiers du Québec (forestry)

- Fédération des producteurs d’œufs du Québec (eggs)

- Éleveurs de volailles du Québec (poultry)

- Les Producteurs de pommes du Québec (apples)

- Les Producteurs de pommes de terre du Québec (potatoes)

- Producteurs de légumes de transformation du Québec (processing vegetables)

- Les Éleveurs de porcs du Québec (pork)

- Producteurs de grains du Québec (grains)

- Les Éleveurs d’ovins du Québec (sheep)

- Producteurs de bleuets sauvages du Québec (wild blueberries from Saguenay-Lac-Saint-Jean and Haute Mauricie only *)

- Les Producteurs de bovins du Québec (cattle)

- Producteurs et productrices acéricoles du Québec (maple products)

- Les Producteurs d’œufs d’incubation du Québec (hatching eggs)

- Syndicat des producteurs de lapins du Québec (rabbits)

- Producteurs de lait de chèvre du Québec (goat milk)

* The Joint Plan covers wild blueberries from the territory of the RCMs of Lac-Saint-Jean-Est, Domaine-du-Roy, Maria-Chapdelaine, Fjord-du-Saguenay and the municipalities of Van Bruyssel, Lac-Édouard, Rapide-Blanc, La Croche, La Bostonnais, La Tuque, Carignan, Lac-à-Beauce and Rivière-aux-Rats in the RCM of Haut-St-Maurice.

To determine the amount of your income from PNACs, we provide you with a calculator (38 KB) * (*Automatic download)

Here are two examples of hypothetical businesses:

Farm with $50,000 in gross income

- Large game production: $35,000 (70% of total income not subject to UPA contributions)

- Maple production: $15,000 (30% of total income subject to UPA contributions)

Since 25% or more of the farm’s income is generated from products not covered by a joint plan, the assessment increase (for $35,000, which is between $0 and $99,999.99) would be $50.

Farm with $360,000 in gross income

- $225,000 from cattle production and $75,000 from grain production (83% of total income subject to UPA contributions)

- Strawberry production: $60,000 (17% of total income not subject to UPA contributions)

Since less than 25% of the income is generated by products not covered by a joint plan, the assessment increase would not apply.

Gross farm income

The definition of gross farm income is primarily based on the definitions of producer and agricultural product in the Farm Producers Act.

Gross farm income is money derived from marketing agricultural products (except wood products). This includes any income producers earn from livestock, as well as any replacement, supplementary, or additional income associated with a specific agricultural product.

| INCLUDED in gross farm income | EXCLUDED from gross farm income |

|---|---|

|

|

3. Farm Income Tier Declaration

All farm businesses must declare their gross farm income by June 30 annually, to determine the dollar amount for the new assessment to be paid the following year.

Simple and quick, the income tier declaration can be completed online by the producer or by an authorized third party.

Find out more This link will open in a new window

Access the declaration website This link will open in a new window

Next steps

- Summer 2026: Analysis of the amounts submitted with the declaration and validation of the prospective scenarios for assessment tiers.

- Fall 2026: Final decision by UPA delegates about the base and supplementary assessment amounts.

- December 2026: Submission to the Régie des marchés agricoles et alimentaires du Québec (RMAAQ) of the proposed assessment amounts associated with each income tiers, including the supplementary assessment.

- January, 2027: The new due system is scheduled to come into effect, subject to RMAAQ approval.

What is the money collected by the UPA used for?

Questions about the new system?

See here for answers.

If you have any further questions,

please contact your local syndicate,

write to us at cotisations@upa.qc.ca,

or call the dues service

at 1-855-534-7120.

Since 1990, assessments charged to producers have been dictated by the legal structure of each farm business (sole proprietorship, partnership, trust, legal person, etc.). The parameters that determine the assessment amount are outdated and no longer reflect the reality of farming today.

Over the past few years, producers have on multiple occasions asked the UPA for the following:

- Assessments based on businesses' gross farm income instead of their legal status

- More equitable financing through a new mechanism to allow for an assessment increase for producers not covered by joint plans

In response to these requests, numerous advance consultations were held. The purpose of these was to see how willing producers were to change the system. November 2023 saw the passing of Bill 28, which amends the Farm Producers Act. As a result, the UPA is now allowed to set new parameters for determining assessment amounts.

Following a rigorous consultation process with members, a resolution of intent was passed at the General Congress in December 2025, that lays the groundwork for a new and more equitable dues system.

Increasing UPA's revenues is not the goal of the new dues system. The system is designed to address financing needs that have already been identified. Under the new proposed system, the amount paid by each farm business will change in order to ensure greater equity.

A portion of UPA financing comes from a variable contribution based on the production volume. Under the current dues system, productions outside of a joint plan do not pay that contribution to the UPA.

The supplementary assessment aims to ensure greater equity among farms, taking into account whether or not they contribute to the UPA through a joint plan. This financing method is comparable to the contributions required for productions under a joint plan, which already provide 35% of the Union's funding.

To find out more about the dues system This link will open in a new window

Yes. The Règlement sur les contributions des fédérations et des syndicats spécialisés à l’Union des producteurs agricoles (Regulation respecting the contributions of specialized federations and syndicates of the Union des producteurs agricoles) continues to apply. The regulation already allows for a certain amount of equity between producers, since contributions paid to the UPA by the specialized federations and syndicates that administer the joint plans already account for the volume of agricultural products marketed.

Yes. All farm businesses in Quebec are required to complete an annual declaration in 2026 so that the UPA can determine the assessment amount they need to pay the following year.

You can complete your assessment tier declaration online via a secure website, or by paper through the mail. You can also contact our dues service for support and to fill out the form with us by phone.

Access the declaration website This link will open in a new window

There are other ways to file your declaration:

- By phone: Call the Contributions Department at 1-855-534-7120

- By mail: Download the form (171 KB) , fill it out, and send it to the address provided.

The annual declaration is mandatory for all agricultural businesses in Quebec. If no declaration is filed, reminders will be sent. If a declaration is still not submitted after these reminders, the UPA will assign a default income tier to the business, based on the information we have on file. The assessment amount for the highest income tier could be assigned.

You will need an official document showing your business's gross farm income for the fiscal year ending in 2025.

- General partnerships (SENC), joint producers (co-ownerships): statement of operations of a farm business (Federal Income Tax Return Form T2042)

- Companies, cooperatives, limited partnerships, and trusts: financial statements

It will be important to use the same type of document for subsequent years' declaration. If a supplementary assessment, to help you determine the amount to be used in the calculation, please download the calculator (38 KB) .

Rigourous consultations were conducted with producers to take into account all requests and individual circumstances. Several scenarios were considered. The one chosen, following the 2025 consultations, addresses the majority of requests for the most equitable dues system for everyone.

Yes, they are subject to a supplementary assessment. Productions with a CCD do not pay contributions to the UPA through their specialized federation. They are therefore considered eligible for a supplementary assessment, based on the percentage of their gross farm income from products that are not covered by any joint plan.

Assessment

The assessment is an amount of money that all producers pay to the UPA each year. Depending on their structure, certain farm businesses pay a double assessment. This is the case when multiple producers are grouped together within the same partnership[SI1] , for instance.

Contribution

The specialized federations and groups that administer joint marketing plans collect a certain amount of money each year from producers within their dedicated production type. This amount is based on each producer’s volume. A portion of this money is used to finance the joint plan itself; it varies based on the collective services delivered under each plan. The remaining portion of the money collected is the contribution paid directly to the UPA by the specialized federations and groups. In sectors not covered by joint plans, producers do not pay any contributions.

Since 1956, the Act respecting the marketing of agricultural, food and fish products has allowed producers to join forces and collectively organize the conditions for producing and marketing their products. This practice is known as collective marketing.

A joint plan is one of the forms collective marketing can take. It allows producers within the same sector to share costs and give themselves the tools they need to carry out their activities collectively. They may, for example, define quality standards, ensure optimal conditions for production, run shared research and innovation programs, launch promotion campaigns for their products, and/or provide buyers with a guaranteed supply.

Question?

Get in touch!

Dues Service

555, boul. Roland-Therrien

Bureau 100

Longueuil (Québec) J4H 3Y9

Phone number : 450 679-0540 Fax number : 450 463-5215